As a result, the usual array of energy and utility companies, alongside a few other firms, are recipients of carbon asset risk proposals in 2019. Resolutions ask about the impact on companies of policies that would keep warming “no more than” or “well below” 2 degrees Celsius, and how they will handle the coming challenges that now are being realized. In addition to several more general proposals, the group of resolutions includes a handful of new ideas and specific resolutions. Proponents have filed 20 resolutions and 11 are still pending; eight have been withdrawn and one has been omitted so far; at least one more SEC challenge is pending.

2-degree scenario analysis: Eight resolutions seek analysis about the potential impacts on the company from a low-carbon economy.

NYSCRF has asked Concho Resources, Continental Resources, Diamondback Energy and Range Resources for “an assessment of the long-term impacts on the company of public policies and technological advances that are consistent with limiting global temperature rise to no more than 2 degrees Celsius over preindustrial levels.” None of the companies has received this proposal before, although a methane proposal at closely held Continental Resources earned 5.5 percent in 2016 and another on methane at Range Resources received 50.2 percent in 2018.

Another variant at Antero Resources and Marathon Oil asks each to “publish an assessment of the long-term impacts on the company of public policies and technological advances that are consistent with limiting global temperature rise to no more than 2 degrees Celsius over preindustrial levels.” Antero previously had a methane proposal, which was withdrawn after an agreement, in 2016, while Marathon Oil reached an agreement that led the Unitarian Universalists to withdraw a climate risk proposal in 2016, after a methane proposal received 36.3 percent in 2015.

Withdrawals—NYSCRF has withdrawn the proposal noted above after an agreement at Concho.

ICCR members also have withdrawn a proposal at two insurance companies—American International Group and Chubb—that said

Given the profound societal impacts of climate change and our company’s potentially critical role in mitigating harm to society, shareholders request that [the company] publish an assessment...of the plausible impacts of a climate change scenario consistent with a globally agreed upon target of limiting warming to well below 2 degrees Celsius, as well as additional scenarios reflecting higher global average temperatures.

The Presbyterian Church (USA) had filed a similar proposal last year at AIG and withdrew it then, too.

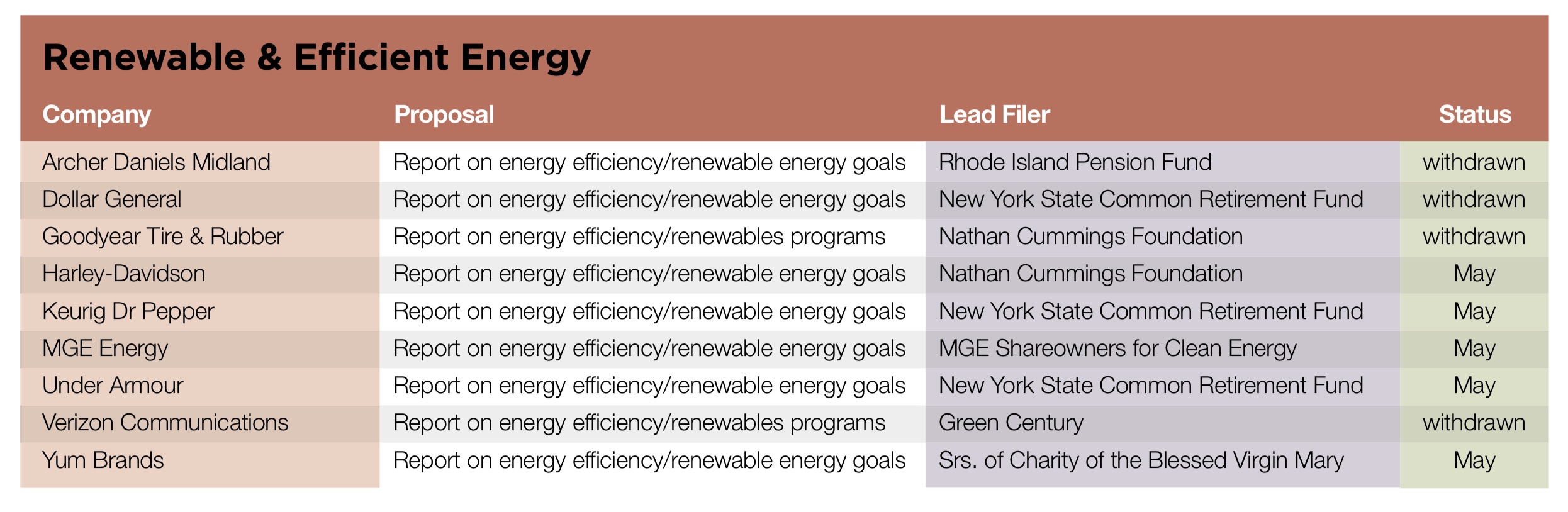

Climate transition plans: Four companies face similar questions about how they will adapt to the challenges of climate change. Proponents at Martin Marietta and MGE Energy want annual reports with “quantitative metrics” where possible or relevant “on the physical and transition risks to and opportunities for the Company associated with climate change,” which “focus on disclosures beyond existing disclosures and beyond those required by law.” NYSCRF says Martin Marietta’s disclosures fall short of TCFD recommendations; it withdrew a 2-degree scenario proposal in 2015 at the company after it reported changes in its cement making business that aim to cut emissions. MGE, a utility in the Upper Midwest, has seen eight proposals since 2015 from its shareholders about renewable energy issues, with the highest vote of 11.1 percent coming last year on a 2-degree scenario proposal.

A group of Amazon.com workers has a new resolution that lists a range of extreme weather events that have affected the company and requests a report “as soon as practicable describing how Amazon is planning for disruptions posed by climate change, and how Amazon is reducing its company-wide dependence on fossil fuels.” In a challenge to a different proposal, the company indicated it plans to include this resolution in its proxy statement. The proposal says the report could include time-bound, quantitative GHG targets. Previously, Amazon successfully challenged a 2018 resolution seeking a report on net-zero GHG goals; the SEC agreed it was too specific and therefore constituted ordinary business.

At Southern Copper, a publicly traded U.S. company with Latin American mining interests, which is a subsidiary of Mexico’s Grupo Mexico, the California Public Employees’ Retirement System (CalPERS) asked for

an annual assessment that is above and beyond existing disclosures and those required by law, which addresses how the Company is managing the physical and transition risks and opportunities associated with climate change. [The report] may cover topics such as governance, strategy, risk management, and metrics & targets.

Withdrawal—MGE produced more information and the proponents withdrew. Ceres reports that CalPERS also received a commitment from Southern Copper, persuading it to withdraw.

Extreme weather: A new resolution from As You Sow asks about potential petrochemical contamination. At DowDupont, the proposal asks for a “report on climate change-induced flooding and public health,” which will “assess the public health risks of petrochemical operations and investments in areas increasingly prone to climate change-induced storms, flooding, and sea level rise and the adequacy of measures the company is employing to prevent public health impacts from resultant chemical releases.” At ExxonMobil, it is nearly identical, seeking an assessment of “the public health risks of expanding petrochemical operations and investments in areas increasingly prone to climate change-induced storms, flooding, and sea level rise” (emphasis added). (See sidebar, p. 30.)

Stranded assets: Two proposals from individual investor Stewart Taggart will not go to votes. Taggart did not provide sufficient proof of stock ownership at Dominion Energy after he asked for a report on “the premature write down, or stranding, risk to the company’s Liquid Natural Gas assets across a range of rising carbon price scenarios,” including “the life-cycle emissions (production, transport and combustion) of the specific natural gas the company delivers as Liquid Natural Gas using various carbon price scenarios and administratively-mandated reductions to meet the 2c target.” He withdrew the same resolution at Sempra Energy after procedural problems with the filing that the company pointed out in an SEC challenge.

Coal: The perennial problem facing carbon-intensive utilities has come up again at two companies. Prompted by a 2014 coal ash spill on the Dan River and breaches of coal ash waste ponds following 2018’s Hurricane Florence in North Carolina, As You Sow wants Duke Energy to “report assessing how it will mitigate the public health risks associated with Duke’s coal operations in light of increasing vulnerability to climate change impacts such as flooding and severe storms. The report should provide a financial analysis of the cost to the Company of coal-related public health harms, including potential liability and reputational damage.” The resolution also suggests the report should discuss how its coal ash disposal affects poor and minority communities. Proponents withdrew a similar 2018 proposal after the company agreed to more disclosure, after a 2017 coal risk reporting resolution earned 27.1 percent.

The Edith P. Homans Trust wants PNM Resources to “identify and reduce environmental and health hazards associated with past, present and future handling of coal combustion residuals and how those efforts may reduce legal, reputational and financial risks to the company,” in a report by January 2020. Several climate change proposals have gone to votes previously at the company, with the highest vote of 49.9 percent coming in 2017 for a request to provide a 2-degree climate change scenario analysis. This is the first coal-specific proposal there.

Gas plant acquisition impact: At MGE Energy, shareholders are concerned about methane emissions from a planned natural gas plant acquisition. They are asking for “a public report within 6 months of the 2019 annual meeting disclosing its strategy regarding their option to acquire 50MW of the 700MW Riverside natural gas plant (Beloit, WI) as it relates to greenhouse gas emission reduction goals, overall environmental policy, and shareholder value.” The company challenged the proposal at the SEC, arguing it concerns ordinary business and the proponents have withdrawn but it is not clear they reached an accord.

Emerging markets investments: A new proposal at General Electric asked for a report on the “adequacy of the company’s climate change related criteria for ensuring that investments in fossil fuel projects in emerging markets are consistent with the Paris Agreement’s goal of limiting global temperature increase to ‘well below 2 degrees Celsius.’” It wanted information about risks associated with new GE investments in fossil fuel projects in Pakistan, Cambodia, Bangladesh, Vietnam, Kenya, and Mozambique. But As You Sow withdrew after a company challenge that contended the resolution concerned ordinary business. The withdrawal came before any SEC response and dialogue on the issues is expected to continue. The company already has provided details on its proposed coal plant in Lamu, Kenya already and set dates for future dialogues about its fossil-fuel related projects in developing countries.